|

Abstract

Purpose – In the context of global New Public Management reform trends and the associated phenomenon of performance auditing (PA), the purpose of this paper is to explore the rise of performance audit in Australia and examines its focus across audit jurisdictions and the role key stakeholders play in driving its practice.

Design/methodology/approach – The study adopts a multi-jurisdictional analysis of PA in Australia to explore its scale and focus, drawing on the theoretical tools of Goffman. Documentary analysis and interview methods are employed.

Findings – Performance audit growth has continued but not always consistently over time and across audit jurisdictions. Despite auditor discourse concerning backstage performance audit intentions being strongly focussed on evaluating programme outcomes, published front stage reports retain a strong control focus. While this appears to reflect Auditors-General (AGs) reluctance to critique government policy, nonetheless there are signs of direct and indirectly recursive relationships emerging between AGs and parliamentarians, the media and the public.

Research limitations/implications – PA merits renewed researcher attention as it is now an established process but with ongoing variability in focus and stakeholder influence. Social implications – As an audit technology now well-embedded in the public sector accountability setting, it offers potential insights into matters of local, state and national importance for parliament and the public, but exhibits variable underlying drivers, agendas and styles of presentation that have the capacity to enhance or detract from the public interest.

Originality/value – Performance audit emerges as a complex practice deployed as a mask by auditors in managing their relationship with key stakeholders.

Discussion and conclusions

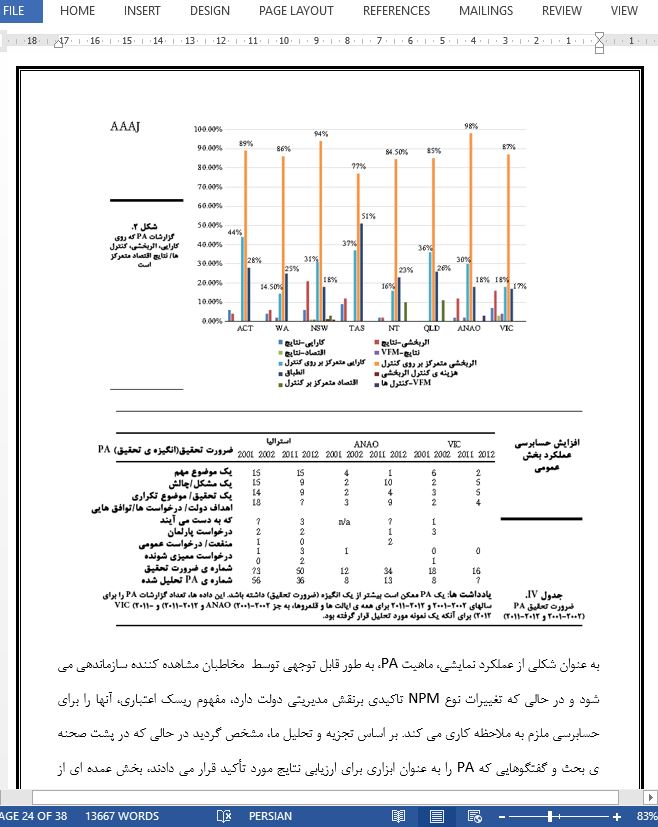

The “middle age” of NPM seems complex and paradoxical, characterised by layers and blends of policy and initiatives rather than clearly defined trends and programs. However, PA has grown to become well established in many jurisdictions in Australia (Barrett, 2011; Guthrie and Parker, 1999). While authors have generally attributed this growth of PA to the output focus and managerialist aspects of performance measurement associated with PA (Glynn, 1985; Free et al., 2013), there have been few examples of analysis of the practice over a significant period of time and across multiple (yet similar) jurisdictions (Pollitt et al., 1999; Pollitt, 2003; Bowerman et al., 2003). This study has involved a comparative analysis of the PA practices across all the Australian federal, state and territory audit jurisdictions.

|

.jpg)

.jpg)

.PNG.png)

.jpg)

.JPG.jpg)

.jpg)

_.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.gif)

.jpg)

.jpg)

.jpg)

نظرات ارسال شده